Out-of-network health care deductibles, copays, coinsurance

KEY TAKEAWAYS:

- Deductible: What it is, and what it means.

- How is a copay different than a deductible?

- What is coinsurance?

Deductibles, copays, and coinsurance, oh my

Every industry has its own jargon — and health insurance is no exception. At Naviguard®, we’re health insurance experts. Helping patients and employers manage the confusing world of out-of-network health care is what we do. We believe the better you understand health insurance, the better you can make smart decisions about your care and avoid costly pitfalls.

Let’s start with how health insurance works

The goal of health insurance is to make health care — which can be quite expensive on an individual level — more affordable. When your employer offers a health plan, you make a monthly payment that allows you to utilize the plan benefits when you get sick or injured.

Because most of us are healthy most of the time, the monthly payments we make when we’re well help cover expenses when we’re sick or injured.

Health insurance plans help manage their own unpredictable costs by negotiating lower, discounted rates with groups of providers. Also, by sharing some of the costs with their members. And that’s where the hard-to-understand terms come in.

What is a deductible

Your annual deductible is the amount you pay in medical costs each year before your health insurance payer (which could be your employer) starts to pay its share. For instance, if your plan’s deductible is $3,000, you’re responsible for paying all your health care costs up to $3,000 within the year, after which your health plan begins to share the cost of covered services.

Deductibles vary from one plan to another and between individual and family plans. Generally, you’ll pay more in month-to-month premiums for a plan with a lower annual deductible, and the opposite is also true. Keep in mind your monthly premiums do not apply toward meeting your deductible.

If your plan includes out-of-network benefits, you’ll likely have a separate, higher deductible if you use out-of-network services — even if you’ve already met your in-network deductible. It’s another reason you’re usually better off financially using in-network providers.

Tip: A higher premium/lower deductible plan can help you better predict your health care costs since you’ll know your out-of-pocket costs can only go so high.

Bonus Tip: If you join a new plan toward the end of the calendar year it may be better to choose the higher premium plan over the high deductible plan, since you’re unlikely to meet your deductible by the end of that year.

What is a copay

A copay is a fixed amount you may be asked to pay up front each time you receive care or fill a prescription. For instance, your insurance plan may have a $20 copay for a doctor’s visit, or a $45 copay for a visit to a specialist, which you’d pay at the time of your appointment. Depending on your type of health insurance, your copays may or may not apply toward meeting your annual deductible.

Some insurance plans offer lower copays in exchange for higher monthly premiums or vice versa (in the same way that a lower annual deductible may be reflected in higher monthly premiums.) For many people, it’s hard to predict which combination will prove the most cost-effective in the year ahead, but your own family’s past health care needs can help guide you.

Do you always have a copay? No. Many plans cover preventive services like mammograms, routine physicals, well-visits, vaccinations, etc. without copays — at least for in-network providers. As a general rule, copays are always lower for in-network providers/services than if you go out of network.

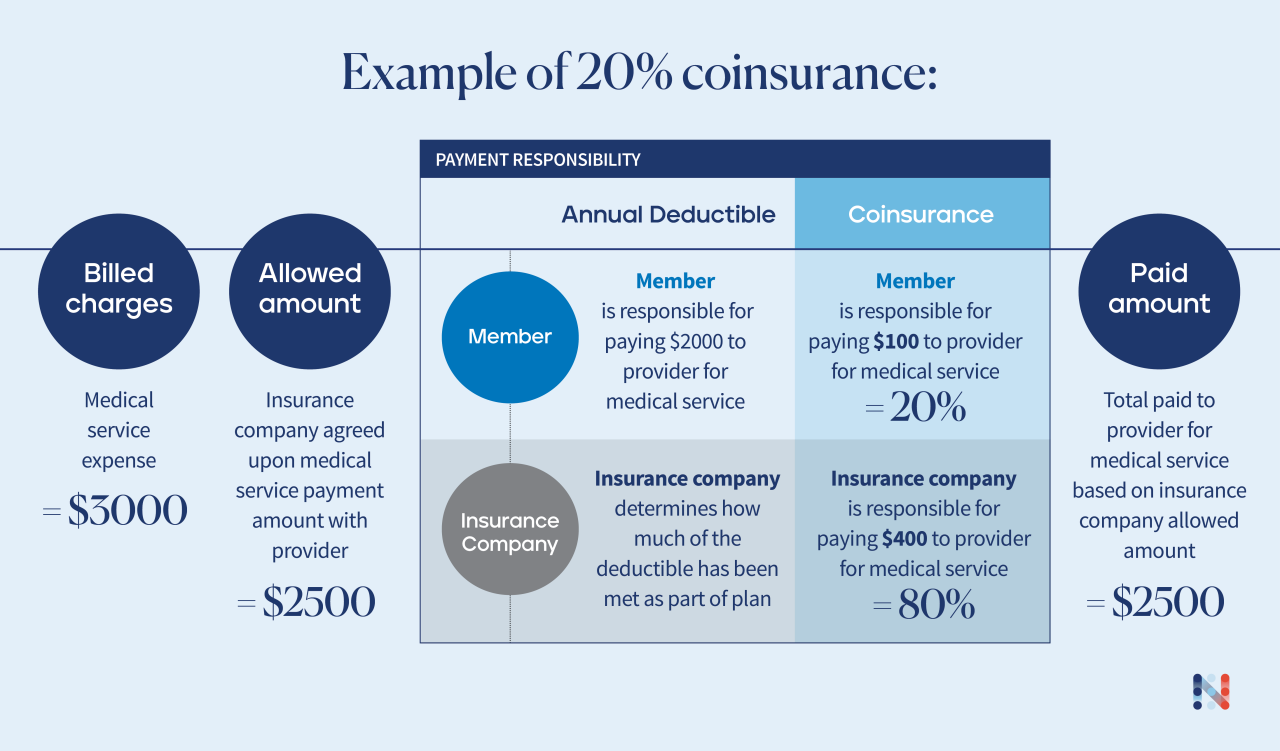

What is coinsurance

Coinsurance is always accompanied by a percent sign — because it’s the percentage you pay of the amount that’s allowed for the service after you’ve met your full annual deductible.

Let’s say your coinsurance is 20%. Once you’ve paid your full annual deductible, you’ll then pay 20% of the allowed amount for the health care you receive, and your insurance plan will pay 80%. What is the allowed amount? It’s the maximum amount on which payment is based for covered health care services.

Your applied deductible + Copay + Coinsurance + Amount paid by insurance = ALLOWED AMOUNT

Good news: there’s a cap

With coinsurance, you’re responsible for a smaller percentage of your medical costs than your insurance company, but the prospect of a massive bill is still daunting. Twenty percent of a lot is still a lot. Luckily, every insurance plan has an out-of-pocket maximum. Once you hit this limit, the insurance company will pick up 100% of your covered costs for the rest of the year – at least for in-network services.

So where does Naviguard come in?

Clearly, health insurance is complex. Naviguard was created to bring clarity to one of the biggest causes of confusion and stress: out-of-network rules and balance billing challenges. We’ve worked with tens of thousands of members and hundreds of employers to successfully resolve difficult, out-of-network balance medical billing issues.

If your UnitedHealthcare plan includes Naviguard our services are available to you at no additional cost. If you get an unexpected out-of-network balance medical bill, especially one that seems excessive, reach out to us for help.

RESOURCES